Layoffs Today, Structural Change, and the Long-Term Demand for Clinical Development

If you look only at recent layoffs, you might conclude that clinical research is contracting.

If you look at the underlying science, capital flows, and patent landscape, you would reach the opposite conclusion.

Both observations are true – and that is the paradox.

Over the past several years, the employment landscape in clinical research has undergone a notable shift. Clinical Research Associates, project managers, startup specialists, regulatory professionals, and other operational roles have experienced layoffs across pharmaceutical companies, biotechnology firms, and contract research organizations.¹ These reductions have extended beyond entry-level roles and have affected experienced professionals and senior managers responsible for overseeing complex development programs.

At the same time, large pharmaceutical companies continue to generate substantial revenues, global R&D investment remains strong, and the need to replenish aging product portfolios has become increasingly urgent.² Having worked alongside sponsors, CROs, and research sites for more than two decades, I have seen similar cycles before, but the current environment reflects something more structural than cyclical.

What we are observing is not a reduction in clinical research activity, but a reconfiguration of how that work is organized, prioritized, and executed.

The Strategic Pressure of Patent Expirations

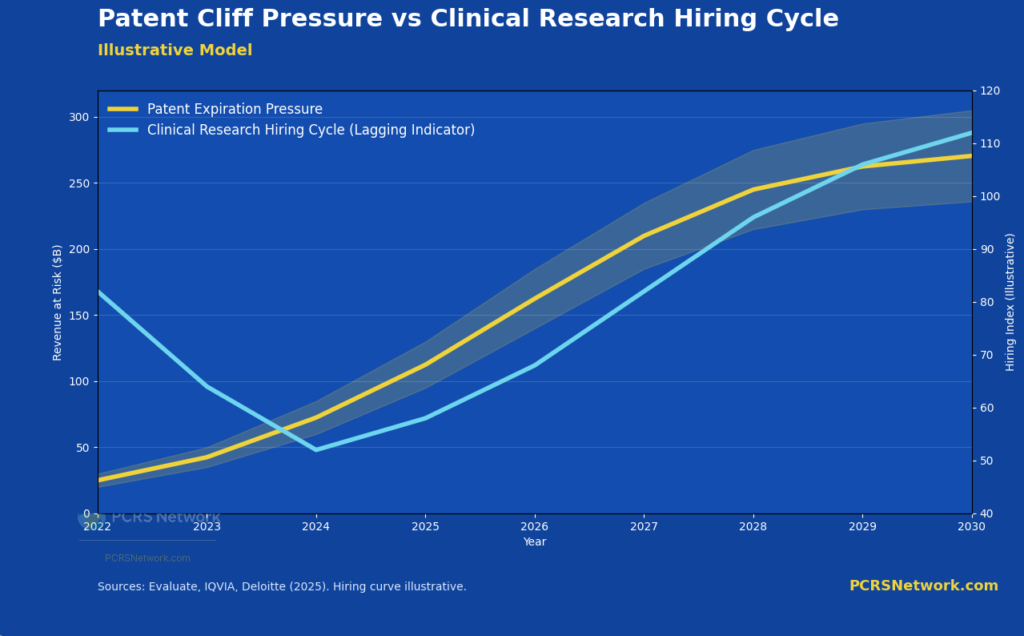

One of the most significant forces shaping pharmaceutical strategy today is the approaching wave of patent expirations affecting high-revenue therapies. Over the next several years, industry analyses estimate that between $200 billion and $300 billion in pharmaceutical revenue will lose exclusivity, exposing these products to rapid erosion from generic and biosimilar competition.³

The implications are straightforward but profound. When a product loses patent protection, revenue declines can occur quickly, often within a short number of years. Pharmaceutical companies are therefore compelled to replace those revenue streams through new product development, expanded indications, or lifecycle management strategies.

Each of these approaches depends on clinical research. New molecular entities must progress through Phase I, II, and III trials. Supplemental indications require additional studies. Even formulation improvements or label expansions typically require clinical evidence sufficient to support regulatory approval.

In practice, this creates a sustained and non-negotiable demand for clinical development. The patent cliff is not a signal of declining research activity. It is a signal of increasing urgency and increasing competition to develop new therapies efficiently.

Explaining the Current Employment Disruption

Given this backdrop, the current wave of layoffs requires a more nuanced explanation. Several overlapping structural dynamics are contributing to what we are seeing.

First, pharmaceutical and biotechnology companies are applying greater discipline to portfolio management. In an environment of rising development costs and scientific complexity, organizations are prioritizing fewer programs with higher perceived probability of success. As a result, assets that might previously have advanced further are now being discontinued earlier, reducing the operational footprint required to support them.¹

Second, the industry is still normalizing after the rapid expansion that occurred during and immediately following the COVID-19 pandemic. During that period, operational teams were scaled quickly to meet accelerated timelines and increased trial activity. As those conditions have stabilized, some of that expansion has proven to be temporary.²

Third, organizational restructuring is reshaping how work is distributed. Companies are reducing management layers, consolidating functions, and reconfiguring global development organizations. In my experience, these changes tend to disproportionately affect mid-level and senior roles that sit between strategy and execution, particularly those focused on coordination rather than direct value creation at the site or patient level.

Finally, advances in technology are beginning to influence operational models. Artificial intelligence and data-driven tools are being applied to feasibility, patient identification, site selection, and regulatory documentation.⁴ These tools are not replacing clinical research professionals, but they are changing how teams are structured and where human expertise is most valuable.

The Evolving Role of CROs and External Partners

At the same time, outsourcing continues to expand as a central component of clinical development strategy. Pharmaceutical companies increasingly rely on contract research organizations and specialized service providers to execute large portions of their programs.⁵

This shift can create the appearance of contraction within sponsor organizations while the overall volume of work remains stable or grows. Over time, employment is redistributed across a broader ecosystem that includes CROs, functional service providers, and technology-enabled partners.

From a practical standpoint, this changes the nature of operational roles. Success increasingly depends on the ability to manage external partners, align incentives across organizations, and maintain execution quality across distributed teams.

Indicators of Underlying Industry Strength

Despite current employment volatility, several indicators point to continued strength in the clinical research enterprise.

Global R&D investment remains elevated, particularly in oncology, immunology, rare diseases, gene and cell therapies, and neurological conditions.² These therapeutic areas are inherently complex and require substantial clinical development effort.

Clinical trial activity has also stabilized following pandemic-related disruption. Trial starts have returned to pre-pandemic levels, and enrollment performance has improved after several years of variability.²

Biotechnology funding, while cyclical, has historically followed a pattern of contraction followed by renewed investment. As capital returns, assets that have been paused or delayed tend to move forward into clinical development.⁵

In addition, large pharmaceutical companies continue to pursue acquisitions and licensing agreements to strengthen their pipelines. Each of these transactions ultimately results in programs that must progress through clinical trials.

Taken together, these factors suggest that the underlying demand for clinical research has not diminished. It has simply become more selective and more strategically focused.

Illustrative model showing how hiring cycles lag underlying clinical development demand, even as patent-driven pressure to replace revenue accelerates.

Implications for Clinical Research Professionals

For clinical research professionals, the current environment requires both realism and adaptability.

In the near term, hiring conditions are likely to remain uneven. Organizations are more deliberate in headcount decisions, and competition for certain roles has increased. Flexibility in role definition, employer type, and geographic scope may be necessary.

At the same time, the long-term drivers of demand remain intact. Aging populations, chronic disease burden, and the emergence of new therapeutic modalities ensure that clinical development will continue to be a critical component of healthcare innovation.

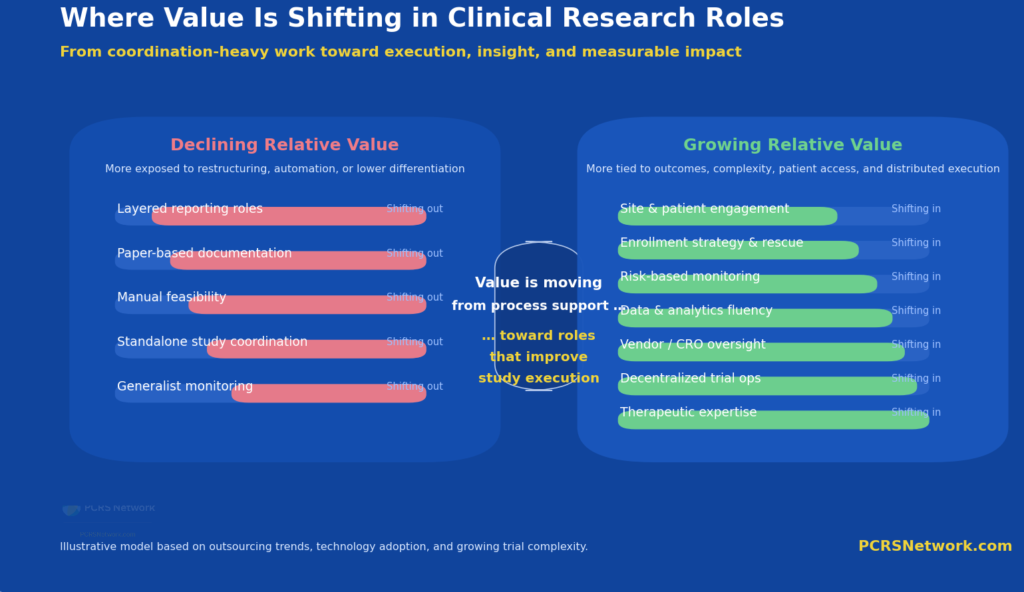

What is changing is not the need for talent, but the profile of that talent. Increasingly, value is placed on professionals who can operate within complex, data-driven environments, engage directly with sites and patients, and contribute to execution rather than solely coordination.

Value in clinical research is shifting away from coordination-heavy roles toward execution, insight, and direct impact on study performance.

A Shift in Structure, Not in Purpose

Clinical research has always moved in cycles, but it does not move in reverse.

The current period reflects a shift in structure rather than a decline in purpose. Pipelines are being refined. Organizations are becoming more efficient. Technology is being integrated into operational workflows. Work is being redistributed across a broader network of partners.

Yet the fundamental equation remains unchanged.

Existing therapies will lose patent protection. New therapies must be developed. Those therapies require clinical trials. And those trials require skilled professionals to execute them.

From where I sit, working closely with research sites and study execution every day, the constraint has never been the need for clinical research. It has always been the ability to execute it effectively at the patient and site level.

That remains true today.

And it is why, despite near-term disruption, the long-term outlook for clinical research, and for those who do it well, remains not only intact, but essential.

Because in the end, clinical research is not driven by hiring cycles or organizational charts.

It is driven by the simple reality that patients are waiting.

#SavingAndImprovingLives

Endnotes

- Fierce Biotech, “Fierce Biotech Layoff Tracker 2025,” Fierce Biotech, 2025.

- IQVIA Institute, Global Trends in R&D 2025: Activity, Productivity, and Enablers, IQVIA, 2025.

- Reuters, “Biopharma Industry Eyes 2025 Bounceback, Grapples with Uncertainty,” Reuters, January 14, 2025.

- Reuters, “Drugmakers Turn to AI to Speed Trials and Regulatory Submissions,” Reuters, January 26, 2026.

- Reuters, “Contract Research Firms’ Strong Earnings Signal Stabilizing Biotech, Pharma Demand,” Reuters, July 24, 2025.